In my previous post: How to compute for the monthly amortization payment without a mortgage calculator, Tyrone of Millionaire Acts asked through his comment: “How about if we don’t have access to the amortization factors table? Is there a way to compute it?”. The answer is yes, and I’ll illustrate how to do it through this post.

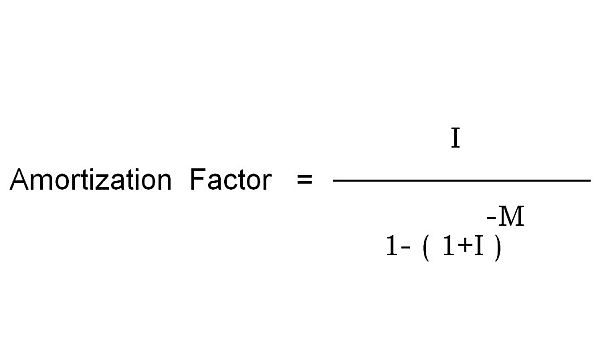

I got the following amortization factor formula when I reviewed for the November 2007 Real Estate Brokers Licensure Exam under Engineer Enrico Cruz:

Where:

I = the monthly interest rate. You can easily get this by dividing the annual interest rate by 12

M = the loan payment term in months. Just multiply the loan term by 12.

Let us use the same example in my previous post.

A foreclosed property is being sold for Php 1 Million and you can purchase it with only 20% down payment, with a maximum payment term of 10 years, at an annual interest rate of 12%. What would be the amortization factor you will use to compute for the monthly amortization?

First, let us compute for the Monthly Interest Rate (I) and the Loan payment term in Months (M)

I = Annual Interest rate/12

= 12%/12

= 1%

M = 10 years x 12 months/year

= 120 months

Now we can compute for amortization factor using the formula above. I’ll just substitute the data below:

1%

Amortization Factor = ———————————–

-120

1 – ( 1 + 1% )

0.01

= ———————————–

-120

1 – ( 1+0.01 )

= 0.01434709

As you can see, we arrive at the same value for the amortization factor we used in my previous example. Of course I would only use the formula in excel as I would not want to compute this by hand, it would be very difficult to calculate for a number with a negative exponent like that in the example right?! 🙂

I would still prefer to keep a copy of the amortization factor table in my wallet so I don’t need to bring my laptop with me everywhere. I can then compute by hand or use the calculator on my cellphone. By the way, I believe there is also a built-in function in excel that can do this calculation but I haven’t tried it yet.

Easy right?!

—

To our financial freedom!

Jay Castillo

Real Estate Investor

PRC Real Estate Broker License #: 3194

Text by Jay Castillo. Copyright © 2018 | All rights reserved.

P.S. – If you are a new visitor, please start here to learn more about foreclosure investing in the Philippines.

P.P.S – If you feel that anyone else you know might benefit from this post, please do share this to them and don’t forget to subscribe to e-mail alerts and get notified of new listings of bank foreclosed properties, public auction schedules, and real estate investing tips.